Alicia Munnell of the Center for Retirement Research at Boston College has a Marketplace column that's critical of the Congressional Budget Office's projections for Social Security's financing, so much so that she places the CBO estimates outside of the "reasonable" range that policymakers should focus on. Is she right?

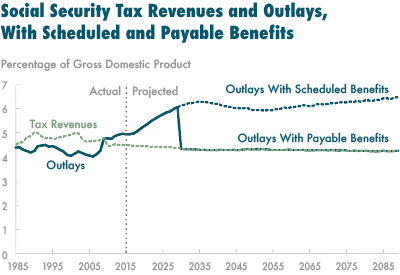

Social Security's Trustees project that the program faces a 75-year actuarial deficit of 2.68% of taxable payroll. For simplicity, that implies that a 2.68 percentage point increase in the Social Security payroll tax -- from the current 12.4% to 15.08% -- would be sufficient to keep the program's trust funds solvent through 75 years. The CBO projects a 75-year shortfall of 4.37% of payroll, which obviously is substantially larger than the Trustees' forecast.

Munnell points to her recent experience heading the Social Security Advisory Board's Technical Panel on Assumptions and Methods. The Tech Panel makes its own recommendations with regard to the main demographic and economic assumptions that drive Social Security financing. Based on the Tech Panel's recommendations, SSA's actuaries scores a 75-year shortfall of of 3.42% of payroll. So Munnell isn't saying that the Trustees projected deficit might not be too low, but rather that the CBO forecast is simply too high to be considered reasonable.

Part of this difference of opinion might come about from a misunderstanding: Munnell points to three areas in which the CBO makes different assumptions than the Trustees: first, CBO assumes greater longevity increases than the Trustees, something which Tech Panels have been recommending for as long as I can remember; second, CBO assumes lower interest rates, which reduce interest earned on the Social Security trust funds. This also is a common area of disagreement, given that current interest rates are so low. Third, CBO assumes that disability benefit claims will continue at higher rates than do the Trustees. I have some sympathy with this argument, given -- as Corner University economist Richard Burkhauser has noted -- the Trustees/actuaries have in the past assumed that relief from rising disability claims was around the corner, but disability continued to increase. While it's not clear by how much CBO's assumptions differ from the Trustees, no one familiar with the process and debates would argue that reasonable people can't disagree on these issues. Having been involved with the Trustees Reports during my time at SSA, there were often people in those meetings who disagreed with where the Trustees ultimately ended up, in ways that would increase or decrease the funding shortfalls.

But Munnell appears to miss another difference of opinion between the CBO and the Social Security Trustees: CBO assumes that earnings inequality will continue to rise, whereas the Trustees assume that after 10 years there won't be any additional changes. Increasing earnings inequality reduces the share of wages covered by Social Security taxes, as well as reducing benefits paid on those wages, but the net effect is to worsen Social Security's long-term deficit. Again, this is an issue on which reasonable people can disagree: my gut is that if health cost increases continue to remain slow, we may see a reduction in earnings inequality. (See this WSJ piece for why.) On the other hard, the Trustees tend to flat-line trends after 10 years due to how SSA's actuarial models are built, which shouldn't be the deciding factor in what's reasonable or not.

It would be nice to see greater detail on CBO's projections, from which we might be able to figure out more precisely what is driving the differences between CBO and the Social Security Trustees. But for now, I don't see any evidence that CBO's projections are unreasonable. The CBO has the more sophisticated model for projecting Social Security's finances and my own view is that the CBO group is more willing to embrace new evidence or thinking as it comes up. That said, as Munnell points out, only time will tell which long-term assumptions turn out to be correct.

If the CBO is right, though, we face a large problem that our political processes are very ill-equipped to address prior to a crisis coming about. That's worrying.

Read more!

Thursday, January 21, 2016

Are the CBO's Social Security projections unreasonable?

Tuesday, January 12, 2016

Upcoming event: “How America supports retirement: Correcting myths about taxes and Social Security.”

Wednesday, January 20, 2016 | 12:30 pm - 2:00 pm

How America supports retirement: Correcting myths about taxes and Social Security

Book Forum

AEI, Twelfth Floor

1150 Seventeenth Street, NW

Washington, DC 20036

Government policy supports retirement preparedness primarily through two mechanisms: Social Security, a mandatory contributory pension for all workers, and tax deferral, which provides incentives for voluntary retirement plans. The combined effect is poorly understood — and subject to widespread myths, including that the current “upside-down” system primarily benefits the wealthy.

Please join AEI as economist Peter Brady presents new research challenging this misconception. In his new book, “How America Supports Retirement: Challenging the Conventional Wisdom on Who Benefits,” he demonstrates that the full system is indeed progressive and warns that tax proposals to limit or fundamentally change tax deferral would make the code less fair. An expert panel will then discuss the myths and facts surrounding America’s retirement system, the power of today’s policies, and the risks of misinformed proposals.

Agenda

12:00 PM

Registration and lunch

12:30 PM

Introductory remarks:

Andrew G. Biggs, AEI

12:35 PM

Remarks:

Pete Brady, Investment Company Institute

1:00 PM

Panel discussion

Participants:

Bill Gale, Brookings Institution

Alan D. Viard, AEI

Moderator:

Andrew G. Biggs, AEI

1:40 PM

Q&A

2:00 PM

Adjournment

Wednesday, January 6, 2016

CBO releases policy options paper for Social Security

In conjunction with its recently updated projections for Social Security’s finances, the Congressional Budget Office has released a menu of reform options for social security.

Given how large a deficit the CBO projects for Social Security – 4.4% of payroll over 75 years, nearly twice as large as the shortfall porjected by the Social Security Trustees – the task of putting together a package of reforms that would balance Social Security’s finances has gotten tougher.

Click here to check it out.

Tuesday, January 5, 2016

Viard: “The Problem with Eliminating the Payroll Tax”

My AEI colleage Alan Viard writes about tax rforms that would eliminate the Social Security and Medicare payroll taxes:

Nobody loves the payroll tax. But, there’s a reason it’s been used to finance Social Security. If we’re going to change how Social Security is financed, we should do it as part of comprehensive entitlement reform.

Until then, let’s stop using the payroll tax as a political football.

Read on to find out why.

WSJ: “New Evidence on the Phony ‘Retirement Crisis’”

In today’s Wall Street Journal, I provide an update on the debate over how to measure the adequacy of Social Security retirement benefits. The recent Technial Panel on Assumptions and Methods recommended a revised method for calculation “replacement rates.” The Congressional Budget Office, right before Christmas, followed up on those recommendations to produce replacement rate numbers using the CBO’s Long Term model. The results aren’t supportive of the idea that Social Security benefits are stingy.

The results are striking: The CBO projects that a typical middle-income individual born in the 1960s and retiring in the 2020s will be eligible for a Social Security benefit equal to 56% of his late-in-life earnings. For individuals in the bottom fifth of lifetime earnings, Social Security replaces about 95% of their substantial late-in-life earnings.

Even so, the CBO excluded the spousal or widow’s benefits that more than one-third of female retirees receive on top of the benefit based on their own earnings. Among retired women who receive these auxiliary benefits, the average total monthly benefit was $1,128, versus $634 based only on their own earnings. In short, the true replacement rates for many retired women are significantly higher than CBO figures show.

Add in 401(k) and other plans, and it should not be difficult for a typical worker to achieve a total replacement rate of 70% or even 80% through individual savings and Social Security benefits.

Check out the whole article here.

Read more!